You have rewards sitting in your account right now. You earned them. You are proud of them. But what if I tell you there is an 80% chance you will never fully redeem them. The bank knows this; the airline knows this. They built an entire programme around this one fact.

What reward points actually are

People assume that reward points are a form of discount. They are not. When you swipe your credit card, the shop you are buying from has to pay roughly 2% as a fee. Your bank takes a portion of that money to buy points from an airline or partner which appears in your account.

These points act as private currency for the company that issued them. These points are not rupees. Hence the RBI does not regulate them. The value is set by the company, and the company can change the value or the expiry date overnight by just updating the terms and conditions.

You are holding a private currency that is not a reward and is fully controlled by someone else.

The word the industry hopes you never Google: breakage

Priya collected 18,000 points over the last three years; she saved them for a ‘special redemption.’ When she logged in last month, she saw that 12,000 points had expired and the remaining 6,000 points got her a ₹150 Amazon voucher or a phone case, which she did not need. She told herself that she would figure it out later and closed the app. Later that night, she swiped her card again to earn more points. The bank had a word for what just happened. They called it breakage. They called it profit.

Globally, 15 to 30% of all loyalty points are never redeemed. That is hundreds of billions of dollars collected from merchants, promised to customers, quietly kept when customers do not redeem them. The five-step verification and the minimum redemption limits: these inconveniences are not an accident. They are intentional, designed to keep you in the system as a continuously spending customer.

The airline secret nobody talks about

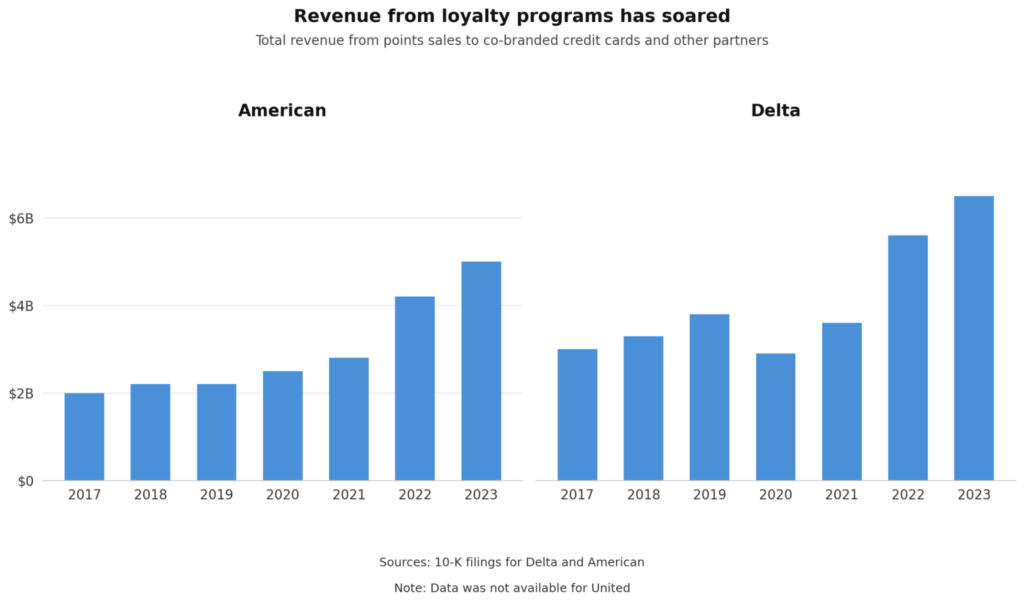

Airlines will never make a profit by flying you from Delhi to Mumbai. Their real business is selling points to banks. Every time you swipe your card, banks buy points from airlines at a fixed rate and pay the cash upfront. You get a number ticking up on an app while airlines get paid real money.

If you redeem, the airline gives you a seat that would have flown anyway. They have already been paid. They win. If you do not redeem, they keep the cash and deliver nothing, which occurs most of the time. They win even more.

During Covid, when airlines were bleeding cash, they did not borrow money against their aircraft; instead, they borrowed against their loyalty programmes. Delta raised $6.5 billion, United raised $5 billion, American Airlines secured $10 billion. The thing they were giving away for free turned out to be their most valuable asset during the crisis.

What happened in India in 2024–25?

Every major bank in India reduced their rewards between 2024 and 2025. HDFC, Axis, American Express all reduced earning rates by capping lounge access, adding minimum spend requirements, and removed transfer partners. A lot of these cuts were made overnight, which shows the level of autonomy these banks have over their loyalty programme.

The starkest example: Air India SBI Signature Credit Card cut its reward rate from 30 points to 10 points for every ₹100 spent on Air India ticket purchases. A 67% slash with no prior notice and no compensation for existing cardholders.

The psychology keeping you hooked

The financial and psychological engineering behind these loyalty programmes is very sophisticated.

- The sunk cost trap: You feel like you have earned so many points that stopping now would be a waste. So you keep spending, not because the reward is worth it, but because stopping feels like a loss.

- The tier illusion: Gold, Platinum, Elite. There is always one tier above you, always one milestone away. These thresholds keep moving, designed to make you chase.

The loyalty programme does not reward you; it conditions you.

The bottom line

Your reward points are a private currency that lets banks change the rules whenever they want. You would never accept those terms from a government, but you would accept them from your bank and call it a benefit.

The programme was never designed to reward you.

It was designed to keep you.

Citations

https://www.reuters.com/world/americas/delta-pledges-loyalty-program-raise-65-billion-2020-09-14

Recent Comments