Introduction

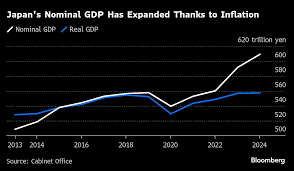

Japan’s economy has been experiencing an economic crisis of low growth in the GDP, averaging around 1% or below in recent decades and was declared as the 4th largest economy in the world by nominal GDP in 2024, yet struggles for productive growth and boost in the economy. This weak growth is part of ongoing structural challenges, including an aging population and productivity constraints.

This has happened due to a series of events since World War 2 where a country and an economy, which was about to beat the US economy, has reached to such a position where growth is not seen, wages are cut and the system is not willing to recover to its full potential.

Economic History of Japan : Post World War

The Japanese economy was in ruins at the end of World War II in 1945. The immediate postwar period involved a challenging notion to rebuild and find stability. The Allied occupation forces implemented land and labor reforms, and American banker Joseph Dodge outlined a plan for a self-sustaining economy. The start of the Korean War in 1950 created a massive demand for Japanese products and sparked an investment push that set the stage for a long period of remarkable economic growth. While investment in factories and equipment grew due to a rising domestic market, Japan also focused on strong export policies. Increased demand for Japanese goods especially in foreign countries led to trade surpluses, which, except for a brief pause in 1979 to 1980, became a regular occurrence by the late 1960s.

The Superpower Aid: Calm Before The Storm

At the start of the Cold War in 1947, the United States saw Japan as a key defense against Soviet influence in Asia. To stop communist expansion and protect its interests, the US provided significant financial aid, security support, and policy assistance to help rebuild Japan after World War II. This partnership set the stage for Japan’s quick recovery

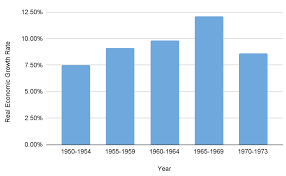

Within Japan, there was strong cooperation between the government and businesses. In 1949, the Ministry of International Trade and Industry (MITI) was created to support heavy industry, manufacturing, and export competitiveness. With help from US technology transfers, access to American markets, and a relatively strong yen, Japan adopted a strategy focused on export-led growth. High domestic savings financed large-scale industrial investments, and a stable job market boosted productivity. From 1955 to 1973, Japan saw remarkable economic growth, particularly in automobiles, electronics, and technology, becoming the world’s second-largest economy by 1968.

The Lost Decade: The Beginning

With strong support from the United States after World War II, Japan became the world’s second-largest economy in the 1980s,[Britannicia] surpassing Germany and France. Its automobile industry took nearly 23% of the US market, and in semiconductors, Japan’s global share reached 51%, overtaking the US. Growing competitiveness raised living standards to the highest levels in Asia.

Financial deregulation fueled Japan’s boom. In 1984, the Ministry of Finance introduced “tokkin” accounts that allowed tax-free securities trading. Firms also raised cheap funds through warrant bonds in London’s Eurobond market. Easy credit and growing investor confidence led to sharp increases in stock and land prices.This was the period when Japan’s asset price bubble was growing rapidly. Banks increased lending based on inflated real estate collateral, which further boosted asset values. This cycle of rising prices and expanding credit ultimately inflated Japan’s massive asset bubble

THE PLAZA ACCORD: The Curse

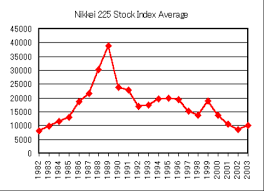

Then, in 1985, during the economic boom, Japan joined other G5 nations in an agreement called ‘The Plaza Accord’. The United States pushed for this accord to fix its trade imbalance with the G5 nations. However, it ended up causing problems for Japan. The Japanese yen was revalued almost immediately and rose sharply in the last quarter of 1985. This posed a serious threat to the Japanese economy, prompting the Bank of Japan to ease monetary policy to offset the effects of yen appreciation. In the mid-1980s, the Bank of Japan cut interest rates to boost exports and growth. Easy credit led to heavy speculation, with firms investing in stocks and real estate instead of productive innovation. Land prices rose over 167% (1985–1990) and stock prices doubled, creating an asset bubble. After the 1987 “Black Monday” crash, tightening was delayed, worsening the boom. When rates were sharply raised in 1989, the Nikkei 225 fell by about 50% by 1992, triggering a prolonged financial and economic crisis.

Post Crash

Japan’s asset bubble burst in the early 1990s, leading to the “Lost Decades” that resulted in nearly three decades of slow growth. After reaching its peak in 1989, the Nikkei 225 fell by more than half by 1992. Land prices dropped over 70% by 2001. Growth averaged about 1%, bankruptcies rose, and wages remained flat.

One major cause was ineffective policy decisions by the Bank of Japan. Interest rates stayed too low after the yen appreciated in 1985. This situation encouraged excessive credit and speculation. When the rates were sharply increased, the bubble burst, causing a credit crunch and a liquidity trap. Deregulating banks worsened the crisis as risky real estate lending increased. After the crash, continued support for “zombie firms” misused capital and extended the stagnation, adding to Japan’s long-term economic problems.

Policy Steps and Central Bank Actions- Insights

The Bank of Japan has historically depended heavily on aggressive monetary policy. In the late 1989-1990, the interest rates increased sharply from 2.5% to 6%. This rise contributed to the collapse of the asset bubble as financial markets reacted quickly. A more gradual tightening might have lessened speculative excess without causing a severe crash and long-lasting deflation.

Although Japan is now recovering, achieving sustainable growth requires more attention rather than just monetary stimulus. Years of deflation and stagnation led to weakened consumption and investor confidence. Given Japan’s aging population, where a large share is more than 65 and tends to spend less, policy should focus on increasing demand. This can be done through creating jobs for young people, raising wages, and improving market competitiveness, rather than relying only on interest rate changes.

This would enhance capital allocation and encourage productive risk-taking. A combined approach that includes gradual monetary normalization, and investment driven by demand is likely to produce better long-term results. In Japan’s situation, both the direction and speed of policy are important.

Conclusion

Japan’s economic journey highlights how rapid growth, financial excess, and policy mis-aligned steps can create long-lasting consequences. The asset bubble and its collapse reshaped the nation’s trajectory, leading to decades of stagnation. Today, careful monetary management and structural reforms remain essential to securing stable, sustainable growth for the future. Slow and steady reforms focusing on consumer-backed demand can help Japan achieve its targeted inflation and steady boost to the economy.

Recent Comments